Source: Freepik

A payment gateway is the first step to getting your money, and picking the right one is critical. Not only will it satisfy your customers and improve your brand, picking the right payment processing system will also save you from a ton of headaches later on.

This article will discuss the best payment gateways in Australia to help your business enjoy the success it should.

Introduction to Payment Gateways for Australian Businesses

An ecommerce payment gateway is one of those things that you don’t think about until you actually begin running your online business in Australia.

It’s an incredibly essential yet often overlooked business process. Perhaps it’s more interesting to consider your innovations, business concept, or your marketing. But processing payments is even more important — it’s how you take e-commerce payments online, and payments are the lifeblood of your business.

According to the Australia Post’s 2024 eCommerce Industry Report, 80% of Australian households bought something online in 2023. Cumulatively, they all spent about AUD 63.6 billion.

Given the massive influx of money to online businesses, how are Aussies paying? According to another industry report by international payment solution PPro, these are the payment methods they prefer:

- Credit and debit cards: 41%

- E-Wallet: 31%

- Bank Transfer: 10%

- Cash: 1%

- Other: 17%

Of those that use e-wallets and digital payment methods, here are the services that Aussies prefer, with the percentage of respondents who’ve used them:

- PayPal: 87%

- BPAY: 61%

- Apple Pay: 39%

- AfterPay: 37%

- Google Pay: 21%

- Payment Express: 4%

- Stripe: 3%

Australians are clearly well-versed in ecommerce payment systems, and they have a standard that you must meet.

But there are tons of e-commerce payment gateways, from international to local ones, which often have tons of features. What things should you consider? Which among the ecommerce payment gateways works best for your business? If you have those questions, the next section will help you decide.

Comparing of the Most Popular Payment Gateways

Like all things in business, your payment processor is not set in stone. You can try stuff out and then pivot if it doesn’t work for you.

However, that doesn’t mean you should just pick whatever the first thing that comes up in your Google search. Knowing what the options are and how to pick the best system for your business will save you time and resources later on.

In evaluating payment gateways, you should ask yourself a few questions:

- What kinds of transactions will you handle? Domestic only, or international? What kinds of currencies will you be dealing with? Does the payment system cater to your merchant accounts?

- How well does it integrate with the top payment systems? A payment gateway should be judged based on how well it works with payment systems. Does it support credit cards like Visa, Mastercard, Diners Club International, etc?

- Is it easy to integrate into your ecommerce platform? Some gateways just require you to install plugins, while others need technical expertise to implement online transactions.

- How much are you willing to pay, and how? Your payment gateway must be making you money, not draining it. Moreover, don’t overlook fee structures. Complicated fee structures are a pain to deal with, no matter the other features.

- What are its security features? Scams are, unfortunately, rampant in Australia, following a long-standing, international trend. Determine what your security needs are, and ensure that your payment gateway has the highest certification for those.

- Is it mobile-friendly? Mobile penetration is nearly 100% in Australia, so not having mobile-friendly features will be a real blow to you.

But most importantly, you need to know what online payment gateways there are, what they’re good for, and what they’re bad against.

Source: PayPal

PayPal

PayPal is practically ubiquitous nowadays. It’s one of the biggest and most globally recognized payment services, with millions of users around the world, including in Australia. It’s certainly one of the most used payment gateways in the country.

Its business mission is set by founder Peter Thiel: to democratize international payments, without going through big banks and other financial institutions.

It has the following advantages.

- Most Australians have a PayPal account: they already use and trust PayPal.

- It offers many robust features for all business types, from credit card transactions to international payments.

- Boasts top-of-the-line security features and high standards for compliance.

However, there are also some notable disadvantages:

- Fees are quite steep just to transfer funds.

- Its fee structure becomes complicated for different services from different countries.

- No white-labeled integration – PayPal payments must redirect to PayPal or have the service’s logo.

For sellers, domestic transactions in Australia cost 2.60% plus a fixed fee (depending on the currency) for regular transactions, while QR codes have a 1.20% fee. International commercial transactions also cost an additional 1% for both standard commercial and QR codes. There are also additional fees for currency conversions.

PayPal is ideal for ecommerce stores that simply want a reliable solution that works and don’t mind complex fee structures.

Source: Stripe

Stripe

Founded in 2010 by the Collison brothers, Stripe has a mission of removing the complexity in online payments that’s present in most other online payment platforms like PayPal. Thus, it focuses on simplifying the integration of payment systems for online businesses, giving them the power to customize Stripe however they want without fuss.

Its main advantages are:

- Straightforward payment structure.

- Highly customizable payment solutions for both desktop and mobile.

- It offers recurring billing for subscriptions and repeat transactions for online purchases.

- Very developer-friendly, with seamless API integration.

- Accept payments internationally with low fees and minimum hassle.

Nevertheless, take note of its potential cons:

- Relatively high fees.

- Technical knowledge is required to leverage the technology fully.

Stripe’s processing fees amount to 1.7% plus A$0.30 for domestic transactions and 3.5% plus A$0.30 for international transactions. However, you can also create tailored solutions with custom prices.

Stripe is best for tech-savvy businesses wanting highly customizable payment solutions, such as startups and international companies.

Source: Braintree

Braintree

A PayPal subsidiary, Braintree is the elevated, high-end online payment gateway version of PayPal. It emphasizes scalability and seamless customer experiences rather than the accessibility that PayPal pushes forward. It also boast its white glove, hands-on support for merchants.

Braintree does the following things best:

- Straightforward fee structures and competitive pricing.

- A full-stack payment gateway and merchant account services.

Nevertheless, it also has a few potential cons:

- Complex payment solutions and integrations are not ideal for small to medium businesses.

- Only email customer support is available, and review sites don’t rate it well.

Braintree’s fees cost 1.75% plus $.30 AUD for every transaction. Custom pricing is also available.

Whereas PayPal focuses on making quick, easy payments for customers, Braintree offers more comprehensive solutions for larger companies with specific needs.

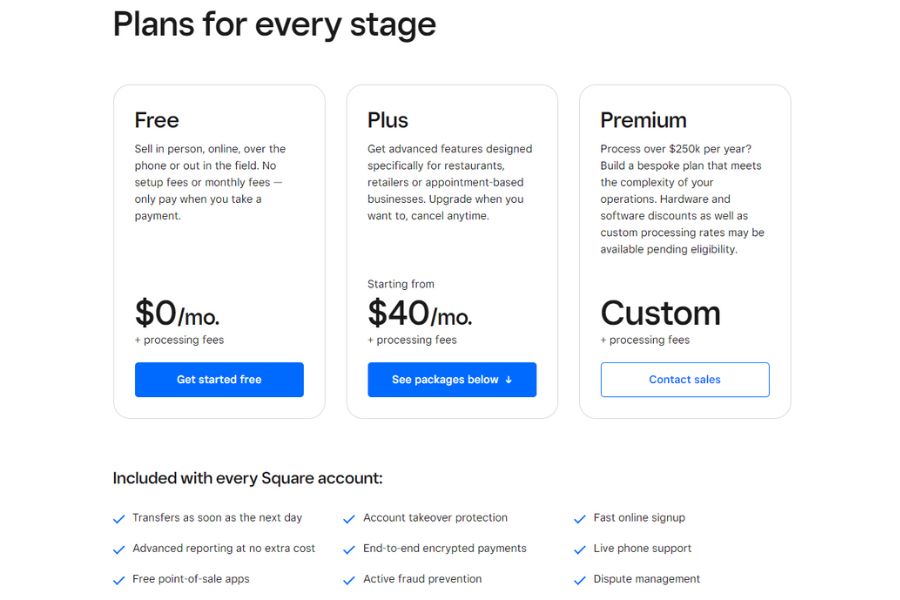

Source: Square

Square

Square, founded in 2009 by Jack Dorsey and Jim McKelvey, is a US-based financial services and mobile payment company. Its mission is to provide easy-to-use financial tools for businesses of all sizes, and thus, it’s renowned for its integrated payment solutions and robust point-of-sale (POS) system.

Here are Square’s main selling points:

- Simplified use for businesses that don’t want to bother with technical details.

- Integrates both online and in-person sales, making it ideal for more business types.

- Supports a variety of online payment methods, including cards, mobile payments, and cash.

- Offers integrated team management, time tracking, payroll prep, and sales feature bundles.

Some potential cons:

- Less flexible customizations compared to some other solutions.

- Limited international transaction support and no cross-border payments available.

- Fees can be higher for some business types.

Square’s payment structure is diverse. They have set transaction fees, which are 1.6% per in-person transaction, 2.2% per online and MOTO transaction, and custom rates for specific services.

However, there are also subscription plans for specific solutions. The first level is free (you only pay per transaction), advanced features cost $40 AUD per month, and custom premium solutions may be priced otherwise.

Source: Square

There are also other specific plans with separate subscription billing, such as fees for POSs, appointments, retail, e-commerce, invoices, terminals, loans, and more.

Square is the best payment gateway for small to medium-sized stores that both have an online and offline presence and who want specific feature coverage for a variety of different situations.

Source: Afterpay

Afterpay

Afterpay is a local Australian BNPL (buy now, pay later) service. Its philosophy centers around providing consumer-centric payment solutions, giving them the flexibility to purchase items through customer-friendly, 4-piece, interest-free installments.

Businesses seek Afterpay for the following reasons:

- BNPL is a highly popular payment method among younger demographics.

- No interest is charged to customers on installments.

- Provides a simple setup for online stores and merchants.

Nevertheless, it’s also limited as a payment gateway:

- Higher transaction fees for merchants compared to traditional payment methods.

- Only supports installments, not full payments.

Afterpay offers interest-free installments for customers, so they make their money through merchant fees. They charge a flat fee of $0.30 AUD per transaction, plus a 4-6% commission.

This payment method is best for retail businesses, attracting younger customers and boosting sales through flexible payment options.

Source: Zip Pay

ZipPay

Another BNPL service, ZipPay, is part of Australian Zip Co Limited. It aims to provide simple financial products for customers. They place a lot of importance on providing transparent offers with no hidden fees whatsoever. For businesses that accept ZipPay payments, customers can pay on flexible weekly, monthly, or fortnightly terms without interest.

ZipPay’s advantages are as follows:

- Customers have more control of their payment schedule, unlike AfterPay, which only lets you pay in one schedule.

- Interest-free payments with manageable fees.

- No setup fees, contracts, or operational fees.

However, it can also have the following disadvantages:

- Fees are per assessment, so some businesses might need to pay more.

- Limited customer credit limit, depending on the approved amount.

Transaction fees go up to 30c per sale, excluding goods and services tax (GST). Specific merchant fees vary according to the company’s assessment.

ZipPay is ideal for businesses wanting to offer no-fuss, transparent, flexible payment options.

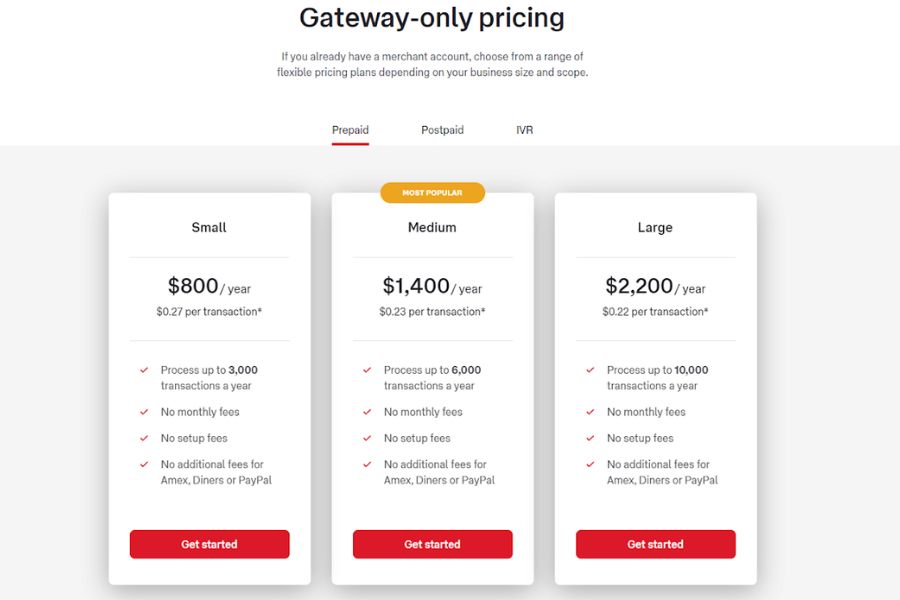

Source: eWay

eWAY

Another popular payment processing service is eWay, an Australian company established in 1998 with the mission to make online payments effortless for Australian consumers. The company prides itself on providing expert, local customer support that makes it so much easier to deal with them.

Here are a few notable advantages:

- Dedicated local Australian customer service, who are available 24/7.

- Ease of integration with over 250 third-party platforms.

- Same-day settlement for transactions.

Here are a few disadvantages:

- High fees for international transactions.

- Additional charges for other services that may not be small-business friendly.

eWay has a couple of subscription tiers, which are as follows:

Source: eWay

If your small to medium-sized ecommerce store is looking for a time-tested, locally-supported service, eWay is for you.

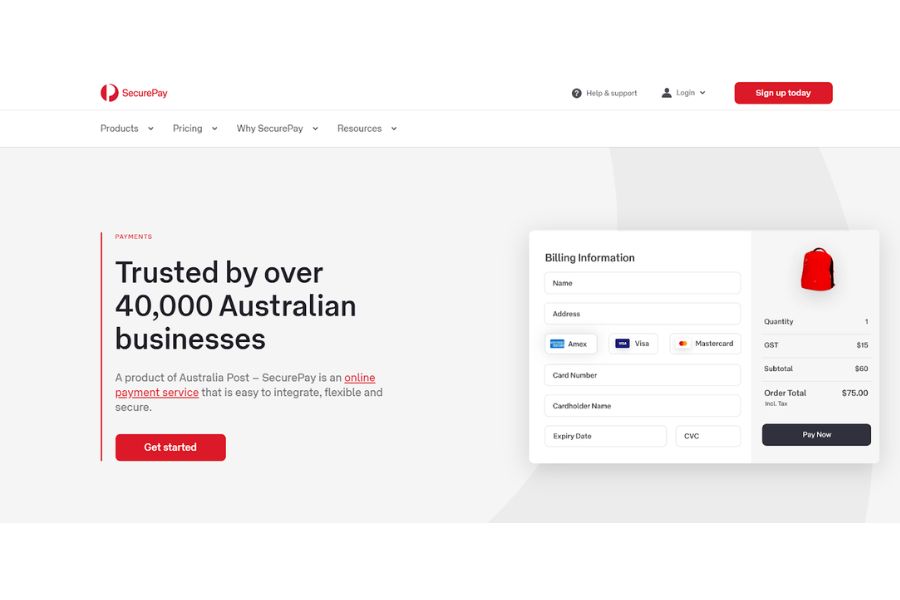

Source: SecurePay

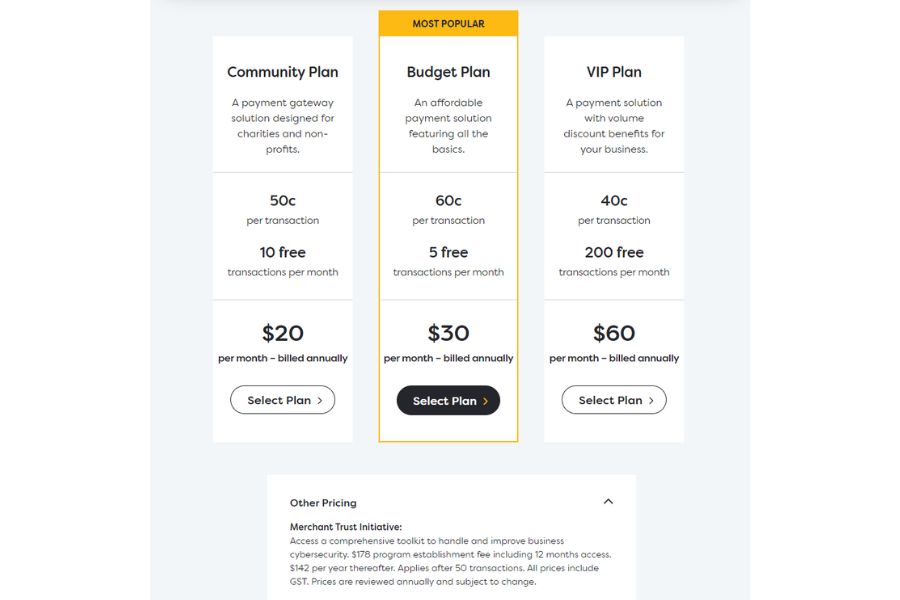

SecurePay

Another long-time Australian payment processor is SecurePay. First founded in 1999 as a subsidiary of Australia Post, it’s now another popular payment gateway you see everywhere. It’s well-known for providing comprehensive solutions for businesses that need multiple types of services to cover all payment channels.

It has the following best features:

- Strong backing from Australia Post makes it a reliable brand.

- Robust local support makes it easier for Australian businesses to use it without fuss.

- Offers both merchant account and payment gateway services through its partnership with the National Australian Bank (NAB).

Its potential disadvantages are:

- Additional services like FraudGuard and direct debit can make it expensive for smaller businesses.

- It may require technical expertise to integrate optimally.

This secure payment gateway offers competitive pricing with a standard rate of 1.75% plus 30c for domestic cards and 2.90% plus 30c for international cards. It also offers gateway pricing, starting at $800 annually for 3000 transactions.

Source: SecurePay

Medium to large enterprises requiring comprehensive payment solutions with strong local support will want to integrate SecurePay.

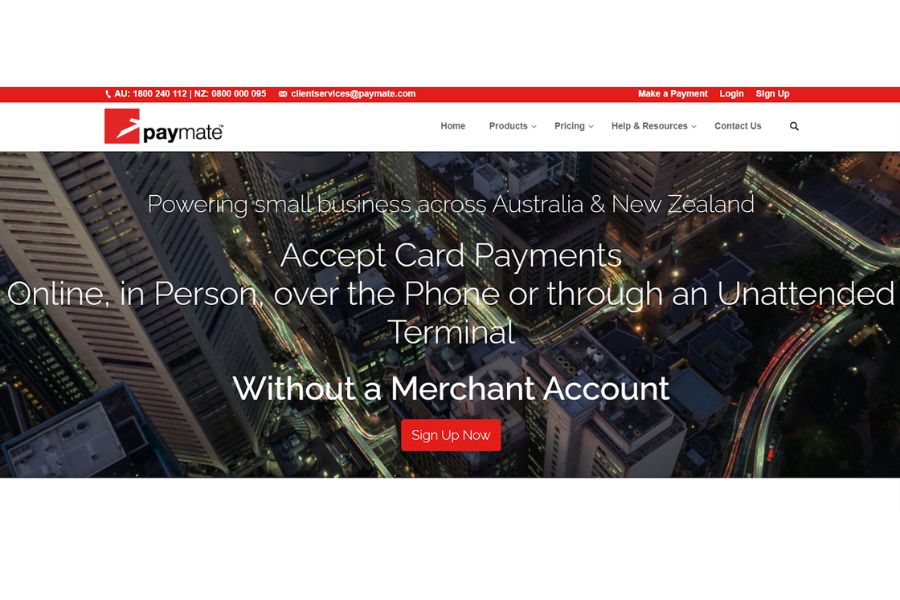

Source: PayMate

PayMate

Originally a Mumbai-based B2B digital payments company, Paymate expanded into Australia, Singapore, and Malaysia in 2023. In Australia, PayMate wants to provide a simple yet powerful payment processing solution that helps businesses succeed in the digital marketplace.

Here are some notable advantages:

- Offers a virtual, integration-free terminal feature for merchants.

- Offers physical, unattended terminals catering to cards for unattended machines (vending machines, etc.).

- Same-day settlement available.

However, there are also some notable disadvantages:

- Higher transaction fees for international payments.

- Don’t really have any advanced features that give it an edge.

PayMate offers a transaction fee of 1.9% per transaction, with an additional 2.75% for foreign currency payments. If you’re looking for a no-nonsense payment system that doesn’t have all the complicated bells and whistles, this is for you.

Source: ePay

ePay

Established in 1999, ePay is an Australian payment provider and a leading provider of prepaid payment solutions and alternative payment processing. It has a vision of redefining bill payments, positioning itself as the leader in Australian transaction-based services.

It has the following best features:

- Offers a comprehensive, 360 solution including integration, all the way to marketing.

- Also offers prepaid payment services such as mobile top-ups, gifting, gaming, and more.

- Strong focus on B2B transactions, particularly from larger brands to retailers.

- Integrates with various point-of-sale systems while supporting popular payment methods.

However, take note of these potential disadvantages:

- The payment structure is highly complex and customized to the business, solution, etc.

- Not for small to medium-sized businesses.

ePay doesn’t have set fees or subscription plans. As it’s a comprehensive, highly-customized solution, their pricing model is based on assessment by their experts.

Consider integrating ePay channels if you want wide coverage for your Australian business or if there’s a specific ePay service that you need.

Source: PaySera

PaySera

PaySera is a European-based payment gateway established in 2004 and has since then expanded operations worldwide. It operates with the vision of making international payments easier and cheaper. It caters to a wide variety of payment methods and offers many other services as well.

Here are some of its notable pros:

- Offers multiple comprehensive solutions, from online payments, contactless payments, to POS systems and ticketing services for events.

- Quick and very reasonable international transfer fees.

- Features contactless card payments and a fast mobile app for secure payments.

Meanwhile, notice these few potential cons:

- Euro-centric operations.

- Limited brand recognition in the Australian market.

- Setup is not as easy as other solutions, requiring technical expertise to integrate some services.

- Complex payment structure for different types of transactions, businesses, and solutions.

PaySera’s payment system centers around Europe, so pricing structure for Australian businesses can depend on a variety of factors. International transfers, however, cost 15 EUR.

Large businesses with many international transactions annually should use PaySera’s gateways, but it’s not that useful for small to medium businesses that focus on domestic transactions.

Source: Adyen

Adyen

Founded in the Netherlands, Adyen is a global payment company with the mission to simplify and accelerate global commerce. Adyen offers a single platform for accepting payments in various secure forms, from online to offline, giving you a bird’s eye view of your resources.

Here are its main advantages:

- Supports payments in multiple currencies, countries, and modes.

- Provides highly detailed insights into your business’ payment data.

- Suitable for businesses of all sizes, from startups to large enterprises.

- There’s a wide degree of available “enhancements,” such as fraud protection tools, revenue optimization reports, etc.

Its main disadvantages are:

- Varying payment method fees.

- Requires a monthly fee for minimum transactions.

- Integration for various solutions can be complex and require technical expertise.

Adyen offers a simple fee structure of a base €0.11 processing fee plus the fees defined by the payment method, which often vary depending on the bank, wallet, etc. There are also additional fees for their enhancements.

For small businesses with plans to grow big quickly, Adyen is a highly scalable payment solution with a global reach.

Source: Alipay

Alipay

Launched by the Alibaba Group in 2004, Alipay is a leading digital payment platform in China. Its business values revolve around safety and security, frictionless use of technology, accessibility, and growth. Alipay is known for its extensive reach in China and its seamless integration with the Alibaba ecosystem.

When incorporating Alipay, you’ll enjoy these advantages:

- Popular among Chinese consumers.

- Advanced encryption and fraud protection.

- Integrates well into smart systems.

However, also take note of these disadvantages:

- It has limited usability outside of China; creating an account requires you to have a Chinese bank account.

- Transactions outside of China are pricier compared to more local alternatives.

Alipay has varying fees for its services. Merchants with a physical POS will pay a rate of 6%. For overseas companies, additional fees for international services and admin may apply.

Given its limited usability, only businesses that serve many Chinese customers often consider this payment method. Service-oriented establishments, such as tourism, retail, hospitality, and international e-commerce businesses, will benefit from Alipay.

Source: Zapper

Zapper: Mobile Payments

Founded in 2011 in South Africa, Zapper is a mobile payment and data insights platform that prioritizes speed of delivery. It combines secure, fast payments with customer engagement for businesses to have a lightweight, all-in-one suite of solutions. It’s available for Aussie establishments to use.

Zapper has the following advantages:

- Offers fast and secure QR code payments, in-person or online.

- Provides detailed analytics of all your transaction data, customer data, etc.

- Offers tools for customer engagement and loyalty programs.

- Simple setup and usage.

However, it also has the following potential disadvantages:

- Limited payment methods, as it focuses primarily on QR code payments.

- More widely adopted in South Africa, with a limited presence in Australia.

Zapper offers varying transaction fees, depending on your subscription.

Source: Zapper

E-commerce and in-person businesses wanting to leverage QR code payments for faster transactions will gain a lot with Zapper. It’s also a good solution if you want to combine fast payment processing with comprehensive analytics.

Source: Freepik

Final Thoughts

Payment gateway providers should be a primary consideration when starting any ecommerce business.

Knowing which services suit your business just right is necessary. Not only is it the only way to process your money over vast, international distances, but it’s also going to significantly affect your customer’s experience in using your ecommerce website.The ecommerce industry is a dynamic and exciting place, but that makes it very competitive. Don’t wait till you’re falling behind to optimize your payment processes.

FAQs

How Can I Choose the Best Payment Gateways for My Ecommerce Store in Australia?

There’s no one answer. The best payment gateways are those that fit the needs of your business. Thus, when choosing, consider factors like its transaction and monthly fees, whether it integrates with popular payment methods such as credit card payments and debit card payments, its ease of setup and use, and its security features.

Are Apple Pay or Google Pay Payment Gateways?

No, they’re not payment gateways. Apple Pay and Google Pay are payment services. They both feature digital wallets and mobile payments. While you can add credit and debit cards, you can’t directly pay with those cards through these payment processors. Nevertheless, they are still an integral part of ecommerce payment processing that brings benefits when implemented the right way.

How Do Payment Gateways Work?

Most payment gateways work the same way. For example, payment processing through one of the major credit cards happens like this: the customer clicks the checkout, the payment gateway gathers information through those fill-in fields and then encrypts the information. Then, the payment gateway sends it to the customer’s bank so the bank can credit the payment to the merchant’s bank account.